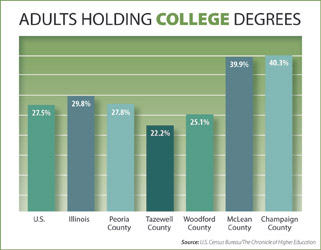

In 2008, U.S. workers with high school diplomas earned an average of $31,283, compared to $58,613 for those with bachelor’s degrees and $83,144 for those with advanced degrees. When multiplied over the course of the typical working life, it’s easy to calculate the monetary value of a college degree.

As a group, college graduates typically enjoy higher job satisfaction, are more likely to receive employer-sponsored pensions and health insurance, have healthier lifestyles, and higher levels of civic engagement, including volunteerism and voting, according to the 2010 State of College Admission published by the National Association for College Admission Counseling. That’s good news for both the individual and the community. No wonder total college enrollment is expected to continue increasing until at least 2018.

Challenges for Schools

But not all the news is good. Colleges and universities are feeling the effect of the struggling economy. During the recession, many private colleges suffered severe losses to their endowment funds, which are used to provide financial aid to students. Now cash-strapped states (including Illinois) have delayed, or even cut, funding for public universities. In an effort to balance their budgets, we’ve seen public universities freeze salaries, cut faculty and staff, and raise tuition dramatically.

Challenges for Students & Families

Challenges for Students & Families

The tuition increases have come just as many students and their families are reevaluating college plans with more weight being placed on financial concerns. Secondary school counselors report seeing an increase in the number of students planning to attend public versus private colleges, to consider two-year versus four-year institutions, or to delay pursuing a degree. Reports from colleges indicate a dramatic increase in demand for student financial aid, just at the time when the budget crisis is causing state legislators to consider suspending or greatly reducing state aid, even for those in the greatest need.

So clearly, college can be a good investment. But finding funds to help pay for college can be more challenging than ever. For many, the question becomes how to find the best college fit academically and socially for the least amount of money. For students and their families, this introduces a whole new set of rules for choosing a college and seeking financial aid.

Federal and state governments allocate their available funds to help students with the most need. Colleges use their funds to build the freshman class they want. That can be based on need, academics, athletics, fine arts talent, community service, ethnic diversity, geographic diversity, balance between male and female, or any number of other criteria that might be important to that school’s mission or vision.

The challenge, as parents try to navigate this complicated process, is to estimate what type of aid a student might be expected to receive and develop a strategy to seek out the schools that will value what that student has to offer. Some schools use their discretionary funds based almost solely on need. Others award their funds based on merit to help shape the incoming class. Some do a mixture of both.

Three Fictional Cases

Justin is the son of two professionals, both with significant annual incomes. Justin’s mother owns a successful financial firm, and the family has significant home equity. Justin’s younger sister is a sophomore in high school. With an Expected Family Contribution (EFC) of $92,000/year, Justin would not qualify for need-based financial aid no matter what school he chose to attend. However, based on his top-10-percent class rank and vocal talent, he could search for colleges that would offer him a merit-based scholarship.

Tamara’s mother is a single parent with three younger children. She works as a CNA at a local hospital and receives no child support. The family has no home equity and very little savings. Tamara has a minimum-wage weekend job at a restaurant, and earns about $2,000/year. With an EFC of $2,600/year, Tamara should qualify for federal grants, and if she is accepted at a school that strives to meet full financial need, she should receive a very substantial need-based financial aid package. She should look for schools emphasizing gift aid that will not need to be repaid rather than loans.

Lauren’s father is a high school teacher and her mother works part-time as a registered nurse. They have a son who is in eighth grade. They have built nearly $100,000 of home equity and have $50,000 in non-retirement savings. With an EFC of $26,200, Lauren will not qualify for need-based aid if she attends her state school where the Cost of Attendance (COA) is $25,900/year. But Lauren would like to attend a private NCAA Division 3 school where she could play softball. The COA at the schools she is considering ranges from $36,000 to $39,000/year. Division 3 schools do not offer athletic scholarships, but Lauren can look for schools that might offer her a service learning merit scholarship based on the after-school tutoring program she established at a local middle school. By looking at schools with a combination of merit aid and need-based gift aid, Lauren may be able to pay about the same at the private Division 3 College as she would at the state school. If she is in the top 20 percent of her high school class, she may even qualify for merit scholarships that would make the private school more affordable than the state school.

So if a student has financial need, it makes sense to seek out schools that have a strong record of meeting 100 percent of demonstrated need. If the family is unlikely to qualify for financial need, the strategy may be to seek schools with generous merit-based scholarships that would be appropriate for that student’s goals and abilities, whether they be academic, athletic, performing arts or some other unique talent. While families are keeping finances uppermost in the decision process, the college with the lowest sticker price doesn’t necessarily end up with the lowest net price. Understanding the financial aid process and developing a strategy unique to each student can be the key to college affordability. iBi

Debra Clay is an independent educational consultant based in Peoria, Illinois, who helps match students with colleges where they can thrive ([email protected]).