As this article goes to press, my busy season is nearly over—while many farmers are just beginning their busy planting season with thoughts of weather and soil temperatures. All the while, their deferred tax liability looms. For cash-basis farmers, this liability is created over time when you defer income to future years and accelerate expenses to keep current income and self-employment taxes low.

Calculate Your Deferred Tax Liability

While commonly used, the potential long-term impact of this strategy is often overlooked. To determine your deferred income position, cash-basis taxpayers should calculate the total of:

– Market value of grain inventory and grain sold on deferred payment

– Prepaid expenses for the next year crop

– Market value of equipment less the undepreciated balance of equipment

– Any crop insurance to be received or elected to be deferred in future year

Next, subtract your current crop year expenses to be paid in the future (e.g., cash rent paid in January for prior crop year).

For most farmers, their deferred income position is a key component of year-end tax planning. As a taxpayer, make sure these two concepts are understood: tax rates and how they might change over time.

Progressive Tax Rates

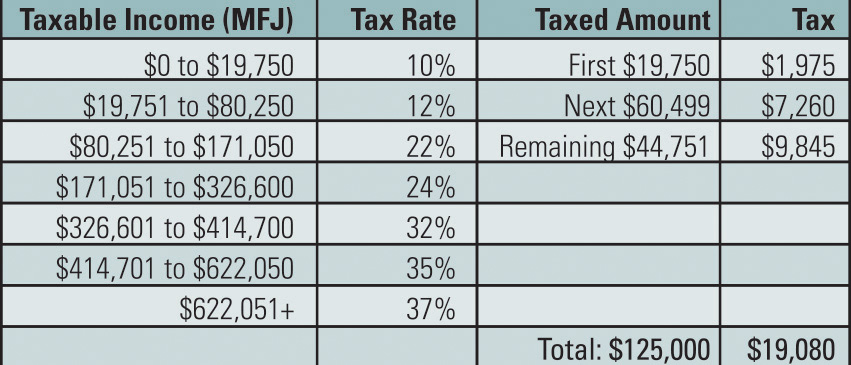

The U.S. federal tax system is progressive (or graduated)—tax rates vary based on taxable income, but each rate applies only to the income within that bracket. To illustrate, let’s imagine someone who is married, filing jointly, and whose taxable income in 2020 was $125,000. Excluding capital gains or self-employment tax calculations, this individual could calculate their tax rate using the following chart:

As each portion of this income is taxed differently, the effective tax rate is 15.26 percent ($19,080 divided by $125,000), with a top marginal rate of 22 percent. Understanding this progressive tax system helps you analyze possible outcomes of recognizing deferred income in one tax year versus spreading it over multiple years. Why? Because you get to use those lower brackets each year on each portion of taxable income.

To illustrate this concept, imagine a deferred income position of $1.8 million. Recognized in one year, each income tax bucket would be filled, leaving $1,177,950 taxed at the top marginal rate of 37 percent. If, however, the income could be spread over three years, the top tax bracket would never be reached—saving more than $140,000.

Potential Changes in Tax Rates

The tax rates listed on the chart are historically low. The Tax Cuts and Jobs Act established these rates—but most of its provisions are set to expire after 2025. In addition to these low rates, the qualified business income deduction is another way many farmers can lower their effective tax rates, while farm income averaging is another tool available to farmers to potentially reduce marginal tax rates. While the future of tax rates is never certain, a new administration paired with an increase in federal spending for COVID-19 relief puts into further question the longevity of these lower tax rates and benefits.

If you are within five years of retirement, develop a plan to decrease your deferred tax liability. Of course, a plan for your income tax considerations is just one component of the retirement, estate and succession planning process. The individual circumstances of your situation should be carefully considered with the assistance of a tax professional. Whether you’re looking to increase or decrease your deferred tax liability—or if you simply want guidance on how to move forward—CLA is here to help.PM

For more information on agribusiness in Peoria, contact David White at [email protected] or (309) 495-6931.

The information contained herein is general in nature and is not intended, and should not be construed, as legal, accounting, investment, or tax advice or opinion provided by CliftonLarsonAllen LLP (CliftonLarsonAllen) to the reader. For more information, visit CLAconnect.com.